ALLCARGO LOGISTICS

Expansion to Play a Vital Role

COMPANY PROFILE

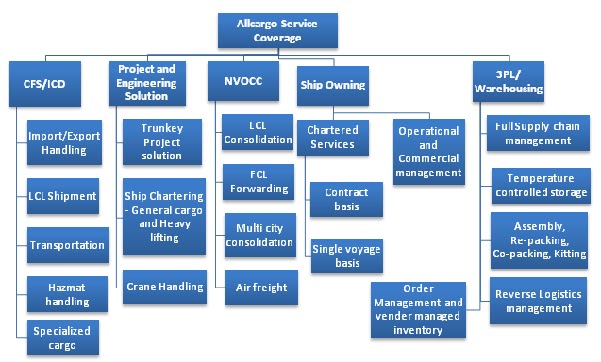

Allcargo Logistics, an Avashya Group company, is among the leading logistics companies in India. The company offers specialized logistics services across Multimodal Transport Operations, Container Freight Station (CFS) Operations and Project & Engineering Solutions as an integral part of its logistics services.

The company currently operates out of 140 own offices in 65 countries and gets supported by an even larger network of franchisee offices across the world. Allcargo Logistics is among India's largest publicly owned logistics companies.

Allcargo Logistics is worldwide leading player in LCL business. Last year the company acquired two Hong Kong based companies engaged in Non Vessel Owning Common Carrier (NVOCC) business in China and other parts of the eastern region.

Today, Allcargo is among the largest operators in the country with world-class CFS facilities in Jawaharlal Nehru Port Trust (JNPT), Chennai, Mundra and Indore. Allcargo cater to the hinterland of North India through its Inland Container Depots (ICD) at Kheda, Pithampur in Madhya Pradesh and at Dadri, Greater Noida in NCR.

ALLCARGO’S CFS/ICD CAPACITY

| Particular | JNPT CFS | JNPT – II CFS | Chennai CFS | Mundra CFS | Kheda ICD | Dadri ICD | Total |

| Nearest port/rail siding | 18 km | 18 km | 7 km | 7 km | 3 km | 0.3km | 12km* |

| Annual capacity (teu) | 144000 | 200000 | 145000 | 48000 | 40000 | 75000 | 652000 |

| Land area (acre) | 28 | 23 | 24 | 16 | 11 | 10 | 112 |

| Warehouse area (m2) | 11400 | 22800 | 14257 | 12210 | 3100 | 5160 | 68927 |

| *: Weighted average | |||||||

INVESTMENT RATIONAL

- Allcargo is world leader in LCL forwarding. It also has a great network spanning world over for NVOCC. Going forward, the company is expanding in segments like ship owning which will help the company’s Multimodal Transport Operations. We observe that the company has maintained top line growth of 25% since last four years and we expect it will maintain same growth in coming years led by the ramp up in the project division and the commissioning of the additional 100,000 TEUs CFS capacity near JNPT.

- Expanding CFS capacity at JNPT to boost growth: With the 2nd CFS near JNPT getting commissioned in 2QFY13, AGLL’s Mumbai CFS capacity will rise to 2.44 lk TEUs. This would boost company’s share at JNPT upwards from the current 7%

- Project order book provides revenue visibility : The Engineering solution segment possesses order book of Rs, 300 cr. which provides revenue visibility for the next three to five quarters.

- Currently the company is trading at 7x of its earning multiple at Rs. 130. We expect the company to report EPS growth of 30% during FY13 and FY14 to Rs. 26 and Rs. 33. We recommend Buy on Allcargo at CMP with price target of Rs. 165 for the time horizon of 12-15 months.

| Price Information | |||

Latest Price (Rs)

|

135

| ||

1 Year Price Var%

|

-2.76

|

Key Ratio

| |

52 Week High (Rs)

|

156

|

Latest EPS (Rs)

|

17.48

|

52 Week Low (Rs)

|

109

|

TTM PE (x)

|

7.74

|

Beta

|

0.48

|

Price/BV(x)

|

1.13

|

Face Value (Rs)

|

2

|

Dividend Yield%

|

1.15

|

Industry PE

|

13.38

|

MCap/TTM Sales(x)

|

0.51

|

Market Cap(Rs Cr.)

|

1725

|

Book Value (Rs)

|

119.8

|

| Financial Highlights (Consolidated) | (Rs. in Crore) | ||||

Description

|

201203

|

201012

|

200912

|

200812

|

200712

|

Equity Paid Up

|

26

|

26

|

25

|

22

|

20

|

Reserve

|

1463

|

1154

|

954

|

558

|

448

|

Total Debt

|

768

|

378

|

204

|

344

|

126

|

Gross Block

|

2153

|

1382

|

924

|

708

|

558

|

Net Sales

|

4271

|

2863

|

2061

|

2314

|

1613

|

PBIDT

|

574

|

298

|

247

|

230

|

147

|

PAT

|

298

|

176

|

141

|

122

|

86

|

Dividend %

|

75

|

150

|

50

|

25

|

50

|

Adj. EPS(Rs)

|

21.86

|

12.71

|

10.41

|

9.63

|

7.56

|

Adj. Book Value (Rs)

|

114

|

90

|

78

|

52

|

46

|

| Quarter on Quarter (Consolidated) | (Rs. in Crore) | ||||

Particulars

|

201206

|

201203

|

YoY %

| ||

Net Sales

|

975

|

854

|

14.18

| ||

Total Expenditure

|

862

|

752

|

14.66

| ||

PBIDT (Excl OI)

|

113

|

103

|

10.69

| ||

PAT

|

59

|

69

|

-14.54

| ||

PBIDTM% (Excl OI)

|

11.64

|

12

|

-3

| ||

PBIDTM%

|

12.12

|

13.14

|

-7.76

| ||

PATM%

|

6.06

|

8.09

|

-25.09

| ||

Adj. EPS(Rs)

|

4.26

|

5.09

|

-16.31

| ||

| Peer Group Comparison (Consolidated) | (Rs. in Crore) | ||||||||

Company Name

|

Year End

|

Net Sales

|

PBIDT

|

PAT

|

EPS(Rs)

|

PBIDTM%

|

PATM%

|

ROCE%

|

ROE%

|

Allcargo Logistics

|

201203

|

4271

|

574

|

298

|

21.86

|

13.43

|

6.97

|

22.7

|

22.34

|

Arshiya Internatl.

|

201203

|

1057

|

279

|

121

|

20.53

|

26.41

|

11.42

|

10.06

|

15.47

|

Gateway Distriparks

|

201203

|

821

|

264

|

136

|

12.19

|

32.16

|

16.51

|

16.07

|

18.92

|